#1-Rated Firm Releases Disturbing Prediction:

The FOUR Horsemen of the

American AI Apocalypse

Why 2026 Could Bring:

• An unprecedented stock market crash

• Rapid hyperinflation of American energy bills

• Hundreds of thousands of white-collar layoffs

• A wipeout of American pensions, 401Ks, IRAs and more …

Dear Reader,

Imagine the worst economic catastrophes in modern American history …

- The Great Depression

- The Dot-Com Crash

- The Financial Crisis of 2008

Each of those calamities brought America to its knees.

Fortunes were lost. Lives devastated. And every day Americans left to suffer at the hands of financial forces beyond their control.

Each was a self-induced economic sickness brought on by the foolishness of arrogant elites.

Now, imagine all three of those things happening — at once.

Could America possibly survive the Mother of All Crashes?

A quick reading of the collapse of great societies would give you a chilling answer:

No.

And yet, the data suggests this calamity could be coming — any day now.

And it’s all because of artificial intelligence.

The hottest buzzword in the stock market could soon be the cause of American doom.

Just look at some of these eye-opening numbers:

- The so-called Magnificent 7 AI stocks — Nvidia, Microsoft, Meta, Apple, Alphabet (Google), Tesla and Amazon — now account for a larger share of the S&P 500 than every single tech stock at the height of the dot-com bubble. A serious warning sign.

- But it gets worse. AI companies have committed to spend nearly $3 trillion by 2028 — while only projecting enough income to cover a fraction of that tab.

- Meanwhile, AI is wiping out middle America — with 300,000 jobs already lost because of AI or AI spending in the last two years alone.

- And AI could cause some Americans electricity bills to spike 70% or more in the coming years.

All of these forces are coming together at the same time to form a perfect storm in the US economy.

Not only could the stock market crash, but we could see massive bank defaults — even a plunge in the value of the U.S. dollar.

Obviously, the pain regular Americans could feel is almost unimaginable.

Unemployment could surge even while the cost of energy and every day goods face hyperinflation.

Retirement savings would evaporate.

Our American way of life would change for the worse.

Now, look … I didn’t send you this note just to scare you.

That is counterproductive in times like these.

Consider this a warning …

A chance for you to act to protect yourself and those you love.

Before it all hits the fan …

Because this could be coming for all of us, whether we like it or not.

Over the next few minutes, I will outline what’s in store for America.

I’ll show you the raw evidence — so you can decide for yourself if I’m right.

In the end, I’m just following the data to its logical conclusion.

But I’ll also show you the best way to protect yourself — and survive the fallout.

In fact, there’s a few small steps to take right now to mitigate the damage.

Smart investors could potentially even prosper in the new economic climate.

But first, let me introduce myself — so I can assure you I’m not just some apocalyptic carnival barker shouting for attention like so many other talking heads.

My name is Nilus Mattive.

I represent a firm called Weiss Ratings. And for the last 100 years we’ve actively warned Americans about every major financial crisis — BEFORE they happened.

Our founder’s father, Irving Weiss, used a series of mathematical formulas to predict the Great Depression.

While the rest of the stock market was drunk on profits, Irving tried to warn everyone he knew that a crash was inevitable — and coming soon.

His bosses on Wall Street scoffed at him. They thought he was trying to ruin their business.

But Irving had the last laugh …

On October 29, 1929, the market dropped 12% — before eventually falling 90% in the next three years.

Irving Weiss — and his small group of followers — not only avoided the crash, but were able to profit during the Depression — even while most Americans were in the poorhouse.

Irving’s son, Martin Weiss, took those well-established formulas and put loads of computer power behind them, creating algorithms to rate stocks, banks and insurance companies.

Today, our team of analysts, mathematicians, and data scientists use his original formulas …

Combined with new formulas and advanced computer models to cut through the financial fog and detect early warning signals.

These so-called Weiss Ratings predicted the bank failures of the Savings and Loan crisis of the 1980s ahead of time, helping followers avoid chaos.

At the height of the dot-com bubble in 1999 …

Analysts at big firms like Morgan Stanley … Bloomberg … or JP Morgan …

Kept issuing optimistic reports with hugely inflated valuations …

And Zacks — a famed stock ratings company — couldn’t find a single stock on the Nasdaq to rank a “Sell.”

But Weiss Ratings signaled something completely different.

It said 90% of all of those stocks were putting investors in great danger …

Sure enough, the dot-com bubble soon followed, wiping out 77% of stock market wealth and ruining the retirements of millions of Americans who failed to heed our warnings.

In 2008, as overleveraged banks loaded up on below-grade mortgage bonds, Weiss Ratings warned of the crisis to come.

In fact, we accurately predicted 98% of the banks who would eventually fail in the Financial Crisis — missing just one.

Consider the big Bear Stearns failure, for example …

On December 3, 2007, we published an alert warning that Bear Stearns … “has sunk its balance sheet even deeper into the hole, with $20.2 billion in dead assets, or 155 percent of its equity, and is threatened with insolvency.”

Bear Stearns collapsed 33 days later.

We also published an article warning that “Lehman Brothers is in similar shape because of an even larger $34.7 billion pile-up of dead assets, or 160 percent of its equity.”

Lehman collapsed 182 days later.

And that single collapse is what ignited the greatest financial crisis since the Great Depression.

We also warned well ahead of time about Washington Mutual, Bank of America, Citigroup and all the major banks that failed or required a bailout.

Weiss Ratings pounded the table for investors, telling them “DO NOT TOUCH THESE COMPANIES WITH A TEN-FOOT POLE” …

While all along, officials on Wall Street and in Washington swore on a stack of bibles that no such failures could EVER be possible.

We know how that played out.

Those who listened to us could have minimized or avoided catastrophic losses … and the personal pain that comes with it, while …

Those who owned the shares in those same big banks saw them plunge 96%, 98%, even 100% from their peak value.

Our Weiss Ratings also signaled danger in 2020, during the early days of the Covid outbreak.

Sure enough, stocks plunged 30% in a handful of days after our warning.

That’s why a study in the Wall Street Journal reported that Weiss Ratings was the #1 stock rating system for profit performance.

When the US Securities and Exchange Commission (SEC) and others commissioned a study to determine which financial ratings company had the best profit track record for stocks …

Weiss Ratings was number one overall.

That’s why hundreds of thousands of investors access our free ratings every day.

While we have a history of spotting danger well ahead of time, I have to say: All of those previous crises pale in comparison to what could be coming, thanks to overblown AI hype.

I believe it’s like the Great Depression, the dot-com bubble and the 2008 Financial Crisis — combined.

And it could change our country for the worse — for years to come.

Already there are signs it could be:

Worse Than the Dot-Com Bubble?

Some of the most common measures of an overheated stock market are flashing red right before our eyes …

Just like they were at the height of the dot-com bubble.

But in this case, the situation could be far more dire.

For instance, right now, just seven AI stocks make up 37% of the total value of the S&P 500.

During the dot-com bubble, the entire technology sector made up just 30%.

Now, take a look at the total value of all publicly traded stocks v. Gross Domestic Product, expressed as a ratio.

Warren Buffett called this, “probably the single best measure of where valuations stand at any given moment.”

During the dot-com bubble, the number topped out at 150%.

But recently, it’s soared as high as 233%.

And yet, the talking heads on TV and your broker are still encouraging you to buy AI stocks lest you “miss out.”

But all of this fear of missing out, or FOMO as it’s called, is what often leads to overvalued, overhyped markets.

When people are worried about missing out, they pile in no matter what the underlying value metrics say.

That’s what happened in the dot-com bubble — when tech investors enamored with the promise of the internet, loaded up … only to see these tech stocks crash 76% or worse, in some cases.

This wiped out the retirement savings of folks across America.

And it took years for them to recover.

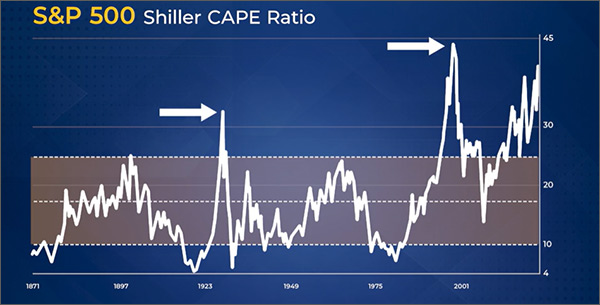

Here’s another potential harbinger of doom for the AI bubble:

Famed economist Robert Shiller’s CAPE ratio – Cyclically Adjusted Price to Earnings – recently hit 45.

That’s higher than the previous dot-com bubble high and 50% higher than right before the Great Depression.

Perhaps the greatest investor in the world, Warren Buffett, sat out the dot-com bubble because of crazy valuations. And now he’s doing the same thing with AI.

In fact, his investment firm, Berkshire Hathaway, has been a net seller of stocks for 12 straight quarters.

Andreesen Horowitz just bet $3 billion against the AI bubble.

So has Michael Burry. He rose to fame in the movie The Big Short. Portrayed by actor Christian Bale, Burry famously said the housing market was going to collapse. And made a fortune when it did.

Now, he’s making big bets against AI. He even shut down his hedge fund because of skyrocketing and unrealistic valuations in the stock market.

“This bubble looks an awful lot like the dot-com bubble,” Burry recently said on a podcast.

Even the CEOs of some of the most popular AI companies are warning about overhyped stocks.

OpenAI CEO Sam Altman, whose company created ChatGPT, said that AI is in a bubble “for sure.”

“When bubbles happen, smart people get overexcited about a kernel of truth,” Altman said.

Sundar Pichai, the CEO of Google’s parent firm, Alphabet, recently told the BBC there is some “irrationality” to the AI boom. And if the bubble bursts, Pichai said:

“… no company is going to be immune, including us.”

Meta CEO Mark Zuckerberg said an AI bubble is “quite possible.”

And Jamie Dimon, head of JPMorgan Chase, told the BBC that he was “far more worried” about the possibility of a crash than most others in his industry.

And while the dot-com bubble was bad for many investors and the US economy as a whole, it paled in comparison to the destruction of the 1929 stock market crash and subsequent Great Depression.

Now, there are signs the coming AI crash could be far worse than even that historic calamity.

Worse Than the Great Depression?

When stocks dropped 90% in three years after the Great Depression, it turned whole industries to trash.

Banks failed, factories shut down and consumer spending sunk to nothing.

The Depression exposed overproduction in agriculture and automobiles, amongst other industries.

Now we’re seeing the same overproduction of AI data centers, and the energy sources used to power them.

If AI stocks were to crash, all of that spending could dry up.

Now here’s what’s really scary:

Harvard economist Jason Furman says investment in data centers and software processing accounted for nearly ALL of US GDP growth in the first half of 2025.

BNP Paribas chief US economist James Egelhof explained, “AI has kept the economy out of a recession.”

AI is “the only source of investment right now,” according to Stephen Juneau, economist at Bank of America.

As you can see on this chart, private business investment excluding AI is mostly flat since 2019.

Commercial construction outside of data centers, of things like shopping centers or office buildings, is down.

If AI spending stopped, how would our economy grow?

As I just showed you, it won’t.

We could see a major drop in GDP and wealth — for many Americans.

Unemployment soared to 25% during the Depression. But AI’s outsized impact on our economy could make job losses even worse.

Already, 300,000 jobs have been lost to AI, either directly or indirectly.

Federal Reserve Governor Christopher Waller recently told a Yale summit:

“We’re close to zero job growth. That’s not a healthy labor market.”

“When I go around and talk to CEOs around the country, everybody’s telling me, ‘Look, we’re not hiring because we’re waiting to figure out what happens with AI. What jobs can we replace?’”

“Everybody’s afraid for their jobs. I’m dead serious.”

We’ve already seen AI stocks with questionable financial numbers sink drastically, like CoreWeave — down 52% in the last eight months.

And Oracle, down 49% in four months.

Now, here’s where it gets really scary compared to the Great Depression …

Back then, in 1929, only 1 in 10 Americans were involved in the stock market.

Now, nearly 6 out of 10 are, including many middle income households through 401ks, pensions and more.

A plunge in the value of AI stocks, and the stock market as a whole, could destroy American retirement, leading to larger consumer spending decreases, especially for an economy that’s on the edge already.

Worse Than 2008 Financial Crisis?

The 2008 spiral of failing banks and government bailouts was caused by lower income Americans falling behind and defaulting on their mortgages.

These risky mortgages were buried inside bank balance sheets and in supposedly “safe” bonds.

Those bonds found their way into pension funds and 401ks.

The chain reaction of low-income mortgage defaults exposed these bonds as garbage and nearly brought the American economy to its knees.

Now, fast forward to 2026 and we’re seeing a similar situation — thanks to the construction of AI data centers.

For instance, OpenAI is planning to spend $1.4 trillion on data centers in the next eight years.

But right now, they’re only booking $20 billion of annual revenue. And there’s no clear path to profit.

In fact, the ChatGPT creator is projecting losses of $74 billion in 2028.

So where is the money going to come from to pay for these data centers, including its massive Stargate complex in Texas?

A consortium of Oracle and Softbank have promised to lend OpenAI $300 billion.

How did they get the money?

Through the bond market.

According to Goldman Sachs, AI-related companies issued $139 billion worth of corporate bonds in the last year …

That’s nearly 10% of ALL investor-grade bonds issued in 2025.

Meanwhile, there are worries about what’s called “circular financing.”

Powerhouse chip maker Nvidia announced it would invest up to $100 billion in OpenAI, who is already one of the largest purchasers of Nvidia’s chips.

Meta is building a $27 billion data center in Louisiana, financed by debt …

Yet neither the debt or the data center itself will end up on Meta’s balance sheets — it’s a magic trick of accounting.

Meta owns only 20% of the debt. The other 80% is held by an investment firm called Blue Owl.

Blue Owl recently sold $27 billion worth of bonds to Pimco, a Main Street fund manager.

Those bonds have found their way into funds run by BlackRock, Invesco and Janus Henderson.

Banks like JPMorgan Chase and Morgan Stanley are rushing to get these AI data center bonds in their portfolios.

Just like the 2008 mortgage crisis or the dot-com bubble before it, no one seems to be considering the worst-case scenario.

What would happen if these data centers failed to pay off and bond defaults rapidly increased?

It could mean drastic results for every day Americans.

Retirement funds, even the supposedly safest of the safe, could plummet. Savings would be destroyed.

Some big banks could even fail.

Would the US government bail them out again?

Who knows?

But either way, lending would squeeze, interest rates would soar — and the value of our dollar could vanish, just like what happened after the Financial Crisis of 2008.

So how will this crash happen?

The First Horseman of the

American AI Apocalypse:

A Drastic Stock Market Crash

Look, I’ve already shown you how overvalued this stock market is against every other historic data point.

In many cases, this data is worse than the dot-com bubble or October 29, 1929.

Here at Weiss Ratings, it seems to us that it’s only a matter of time before the market crashes.

But when will that be?

Obviously, predicting the exact date and time of a crash is a fool’s errand.

I won’t insult your intelligence by pretending to know exactly when this will happen.

Instead, I can show you why it’s coming …

And unfortunately, these days, there’s a heap of reasons we could see the market tank.

I’m talking 75%, even 90% like the Great Depression.

The stock market is currently a top-heavy house of cards — and it’s built on some massive assumptions about AI.

Assumptions that have not paid off yet — and maybe never will.

So what could cause the AI dominos to start falling?

We’ve already gotten a preview.

- Potential crash impetus #1: A Chinese breakthrough that throws all expectations for AI into question.

Do you remember Deepseek?

It was a Chinese AI company who released a report that it could perform the same tasks as ChatGPT — without using Nvidia’s most expensive chips. And without the same power needs as American AI data centers use.

In fact, it claimed to do it a fraction of the cost. Just $5 million, compared to the trillions US companies are spending.

This was in January 2025 — and AI stocks took a deep hit.

Investors faith in the future of American AI was shaken.

The technology sector of the S&P 500 lost over 5% in a matter of hours.

Nvidia fell 17% ...

Chip stocks like Broadcom and Micron fell over 10% ...

Eventually, investigation found a lot of holes in Deepseek’s story of a Chinese AI breakthrough.

But the next time might be the real deal.

And if investors — especially institutional ones — decide we don’t need all of these data centers or AI spending, you can expect them to dump AI stocks rapidly.

Because of AI’s prominent place in the market — it’s essentially the only driver of growth —the chain reaction could see stocks of all shapes and sizes fall quickly.

- Potential crash impetus #2: Geopolitical actions that destroy faith in AI and America’s future.

Then there’s the potential long shot chances … Massive global geopolitical disruptions, either in the form of tariffs, far away wars or the worst-case scenario: A global war involving the United States.

Gone are the days when these fears sounded farfetched.

Unfortunately, nowadays, the threat is all too real.

In fact, The Atlantic Council’s Global Foresight Survey asks hundreds of experts about the prospect of World War every year.

And in 2025, over 40% of respondents believed a World War was coming.

That’s up from just 25% the year before.

And we’ve already seen how the stock market has reacted to the ups and downs of Trump’s first year in office.

With AI stocks already reeling from the Deepseek revelations, Trump announced so-called “Liberation Day” tariffs on April 2, 2025.

The market reacted swiftly.

The Nasdaq tumbled 15% in less than a week.

Stocks like Nvidia and AMD — typically AI strongholds — fell 15% and 24%, respectively. In less than a week.

Now, the market recovered when Trump backed off some of these tariffs, but the threat remains.

And these were minor shocks.

Now imagine if China invaded Taiwan, where much of America’s AI chip production is located.

Access to high-powered semiconductors and valuable rare earth metals could be choked off, delaying the data center buildout.

Worse yet, what if the US felt obligated to protect Taiwan and engage in a head-to-head war with China?

AI stocks would plummet — and the rest of the market would follow.

So again, while we don’t know the exact date the market will fall…

There are a lot more reasons for a crash then there are for another boom.

After all, since the release of ChatGPT in November 2022, Nvidia has gone from a $405 billion market cap to $4.5 trillion.

To do that again would make them a $50 trillion company.

If that’s not an indication of an AI bubble, I don’t know what is.

Ok, so the stock market — led by AI stocks — crashes dramatically.

What happens next?

The Second Horseman of the

American AI Apocalypse:

Bond Defaults, Bank Failures and American savings wiped out.

If the market crashes because AI’s hype is finally exposed, the chain reaction will be swift and brutal.

Remember all of that circular financing I told you about earlier?

Those bonds could get exposed as worthless quickly, especially if the promise of AI revenue dries up.

Many of these bonds will default — and the banks left holding the bag could be in big trouble.

Just like Bear Stearns and Lehman Brothers in 2008.

Back then, the issue was so-called CDOs or Collateralized Debt Obligations…

Souped-up bonds that held some A-grade mortgages, but mostly C or below.

When the mortgages went bust, it had an outsized effect on the entire market.

History tells me if this many high dollar bonds default, the ripple effects will touch everyday Americans.

Some banks, even the biggest in the country, could collapse and fail under the weight.

Lending for businesses and regular Americans might completely dry up ...

Interest rates will rise, stifling the economy.

Then there is the issue of 401ks and pension funds — the cornerstones of retirement for most middle-income Americans.

These AI bonds have been packaged and resold to big investment firms like Pimco, BlackRock, JP Morgan, Morgan Stanley, Invesco and more.

Those are the companies who run retirement offerings for 30% of all Americans.

And with savers clamoring for higher returns, you can bet retirement accounts across all banks are heavy with exposure to AI. Not to mention ETFs, mutual funds and more.

When the music stops and the revenue dries up — who will pay the bill?

The American people. With drastic consequences.

Obviously, losing 50% or more of retirement savings will lead to belt-tightening, at worst.

Consumer spending will drop dramatically, putting more pressure on a struggling economy.

And defaults on credit cards, car loans and mortgages will likely skyrocket, just as they did in 2008.

Already, even before a crash, many Americans are struggling to pay their bills.

Delinquencies on car loans and mortgages have been quietly rising. A tick up in interest rates would likely only make that worse.

Just as Americans are struggling to pay for their homes and transportation, there could be another whammy.

The Third Horseman of the

American AI Apocalypse:

Massive unemployment

We’re already seeing huge job losses because of AI.

Nearly 300,000 jobs were lost because of AI in the last two years.

And that’s before Amazon just announced another round of cuts — 10% of their white-collar workforce.

Companies outside of tech have severely limited hiring, as AI creeps into everyday jobs.

Keep in mind, we’re not talking about people at the bottom of the economic food chain.

We’re talking about white collar workers: people making six figures or more.

Folks who own nice cars, have high-priced mortgages … and lots of credit card debt.

What happens when they lose their jobs and can’t pay?

The already struggling banks could collapse under the weight.

Right now, the struggling jobs market is offset by data center related-jobs in construction, semiconductors and servers, and energy-related work.

But what happens in an AI crash, where many of the most promising companies go belly up?

It’s hard to project, but we could see unemployment reach Great Depression levels — 25% or more.

It’s a double whammy from AI.

Because the technology will likely continue to replace many white collar workers.

At the same time, as the money dries up at some AI companies, more and more jobs will be lost.

A precipitous drop in consumer spending will lead to even more job losses outside of AI, from construction to retail to hospitality.

With loan defaults already accelerating, massive new job cuts will push things over the edge.

The banking crisis will become existential.

And the plunge in U.S. spending will hit international markets as well.

Governments will react by trying to hand out money, lower interest rates and inject liquidity into the system.

But this could have drastic consequences as well.

Rapidly increasing inflation could become hyperinflation.

And unemployed Americans, whose retirement savings were wiped out, will see the cost of everything rise.

Especially energy.

The Fourth Horseman of the

American AI Apocalypse:

Soaring energy bills that bring

America to its knees.

The problem with an AI stock market crash is that it won’t be the end of AI.

AI data centers will continue to operate.

And these data centers are massive power hogs.

In fact, one giant AI data center uses as much power as a city the size of Denver or Boston.

But it’s everyday Americans paying their bills.

Electricity consumption from AI data centers is expected to grow 5x by the end of the decade. And half of that growth is expected to happen in the United States, according to the IEA.

Already, residential electricity prices are spiking in the U.S.

And according to the Century Foundation, surging energy bills are pushing households deeper into debt.

That’s before future increases could be as high as 70% in certain parts of the country.

John Quigley, a senior fellow at the Kleinman Center for Energy Policy at the University of Pennsylvania, pointed to the “data center frenzy” as the primary driver of higher electricity prices for households.

Quigley said, “They’re pretty much the whole boat when it comes to increases in electricity demand.”

And he added ...

“It’s going to get worse.”

Two of the states hit hardest by rising bills, Virginia and New Jersey, saw liberal governors promising to lower prices sweep into office in November.

With bills already rising, combined with hyperinflation and job losses — many Americans could literally see the power go out.

So, what could the long-term consequences be?

An Unrecognizable America

We like to think of the Constitution and American democracy as a special case, making our people unique to those around the world.

But when our economy fails us, Americans will react like every other nation facing an existential financial crisis.

The first step will be to turn to the government for help.

And this could have devastating consequences for the future of our democracy …

Plus, if history is any indicator, these desperate, government-driven solutions will only make the economy worse. And plunge our country into ruin, potentially for generations to come.

As we saw in the Great Depression, and again in the 2008 Financial Crisis, when 25% or more of the country is unemployed, and large groups of Americans are struggling to pay their bills … the government bails them out. Or at least it tries to.

But we’re already facing a $38 trillion national debt …

So where will the money come from?

Well, first you need to understand the potential ramifications of economic collapse.

I see it playing out like this.

Right away, free market governments will be washed away.

Replaced by left wing leaders in favor of government intervention and expansion.

Already, we’re seeing a rise in socialism in the United States — on par with the largest surge in US history, which came right after the Great Depression.

New York City, the center of American commerce, is run by a socialist.

And it’s very possible socialist leaning candidates — politicians who favor large social safety nets and government handouts — will make advances in the coming midterms.

That’s before we’ve even had a serious crash.

Americans are right to be concerned about rapidly decaying economic conditions. And a larger gap between haves and have nots in the so-called K-shaped economy.

But, reaching for the sweet sugar of socialism will turn an economic blaze into a raging forest fire that destroys any wealth in its path.

Because all of this government spending and bailouts of both banks, companies and regular Americans will require money from somewhere.

So who’s going to pay the bill?

You and me.

Responsible, successful Americans who have saved their money and invested wisely.

Because these socialist governments only have a few tricks up their sleeve to produce that money.

And all of them are bad for us.

Obviously, the government and the losers in this crash will immediately blame the wealthy.

They’ll mean the ultra-wealthy. The billionaire elites who mismanaged the AI bubble and data center spending.

The people who run these AI companies and big banks, unchecked.

But instead, they’ll come for you and me — the regularly wealthy, with six or seven figures in assets.

And they will come for us in the form of outrageously high taxes on everything.

Income tax, property tax, capital gains, estate tax …

All of these will rise rapidly, in order to pay for government handouts to less fortunate citizens.

Worse yet, because of recent actions like FedNow and the Clarity Act, funds may be digitally ringfenced by the government.

Meaning they’ll be able to deny any movement of money. And they’ll be able to collect extra taxes from you whenever they want.

If you haven’t acted ahead of time to protect your wealth, you’ll be caught in the crossfire, with no escape.

In a moment, I’ll show you some specific actions you can take to protect your wealth, right away.

But, keep in mind, it’s not just high taxes that will punish you.

The government, through the Federal Reserve, will inject massive amounts of liquidity into the market.

You remember “quantitative easing”?

This will be like that — on steroids.

The government will use every lever at its disposal to print money and pour it into the system.

And the consequences will be disastrous.

The value of the US dollar will plummet as inflation soars, perhaps even reaching hyperinflation levels.

In the Weimar Republic, hyperinflation led to the value of the currency changing rapidly, sometimes multiple times a day.

America could see itself in the same situation.

Except right now, the US dollar is the world’s reserve currency.

That makes our money exceptional and gives us a lot of benefits in world markets.

Oil is priced in dollars.

Other countries and investors buy our treasury bonds for safety and profit.

What will happen when the dollar is no longer the most trusted currency in the world?

Treasury bonds will fall off a cliff. Central banks and institutional investors both inside and outside America will dump them in droves.

Already, there’s evidence of this happening.

The central bank share of treasury bond holdings dropped $48 billion in the first few months of Trump’s presidency.

China’s holdings are at their lowest level since 2008.

India dumped $50 billion in treasuries in just a year.

And that’s before a true economic crisis has hit.

Once investors lose faith in the US government’s ability to pay its bills, the dollar will lose its status as the global reserve currency.

And the value of everything attached to dollars will sink to even lower levels.

The result is almost hard to fathom to us these days.

But it will mean severe punishment for American savers and anyone holding dollars.

In the long term, generations of Americans could live in poverty, with little hope of improving their situation.

The American dream would be dead for the vast majority of the country.

Now, I know the picture I’ve painted here is a scary one. And right now, with the stock market still near all-time highs, it may seem a little drastic.

But the possibility of a crash is at its highest.

I’m sure you can feel it too.

Sensible Americans are starting to ask serious questions about AI hype — and the possible negative consequences.

However, there is a way we can protect ourselves.

And the time to do it is right now.

Don’t wait until the dominoes start falling.

It’s time to take action.

So what can we do?

Well, in every crisis Weiss Ratings has accurately predicted ahead of time, we’ve also recommended the same thing.

Physical gold.

In every crisis in American history, it’s not only kept its value, but grown.

And already in the last year, gold has reached all-time highs.

In fact, just three months after hitting an all-time high of $4,000 an ounce … gold surged past $5,000.

But I think it still has a long way to go from there.

There’s one problem, however.

Most people will buy gold the wrong way.

Don’t Make This Gold Mistake

For nearly 100 years, Weiss Ratings has recommended gold to counterbalance ineffective governments and worthless dollars.

Like Irving Weiss in the Great Depression.

Watching the government print more and more money, Irving started loading up on gold.

At the time, you could buy it for just $20 an ounce.

Everyday Americans didn’t care much for gold. They preferred to keep their money in bank accounts and stocks.

So when the market crashed in 1929, many lost everything.

The average stock tanked 90%. And it took decades for the market to recover.

Folks who entrusted banks with their savings didn’t fare any better.

Between 1930 and 1933, half of the banks in America failed — wiping out the lifetime savings of millions.

Meanwhile, gold, did exactly what it’s supposed to do in times of chaos.

Protect hard-earned wealth.

In fact, no other asset held up as a store of value like gold during the Great Depression.

By 1934, the same amount of gold got you twice as much real estate as before the crisis.

The same thing happened during the massive inflation of the 1970s.

Gold rose from $38 to $612 — a 1,500% rise.

And during the 2008 Financial Crisis, when gold rose from $696 to over $1,900 for the first time.

Now, the same thing is happening.

Savvy investors are aware of the potential pitfalls of AI.

On top of the swirling geopolitical winds of change.

And they’re snatching up gold at a record pace.

Gold prices have soared from under $2,000 in 2024 …

To a record-high $5,417 in early 2026.

Now, another force beyond just Wall Street elites is pouring money into gold.

I’m talking about central banks, around the world.

Central banks were net sellers of gold until 2010, as you can see on the chart. But in the last 2-3 years, central bank gold purchases have surged.

China’s central bank has steadily increased its gold reserves for 14 months straight.

The Wall Street Journal said:

“Central banks in countries that have strained relationships with the West, including China, have been shifting away from dollar-based assets into gold, which is beyond the reach of foreigners.”

Juan Carlos Artigas, head of research for the World Gold Council, added:

“Central banks are buying gold not just purely for its price performance, but the role that it can play in foreign reserves. Gold is very useful to hedge or diversify the reserves.”

Here at Weiss Ratings, we predicted gold’s current rise.

And we don’t expect gold’s price to drop any time soon.

If we see a major market crash in AI stocks, we could see gold double or triple from here.

But what’s the best way to buy gold?

Should you just run out and grab as many gold bars as you can get?

Maybe if you’re a central bank or a billionaire investor.

But for regular folks, that is NOT the way to do it.

There’s a better way to buy physical gold over the long term.

This unique method, which we have spent years studying and perfecting here at Weiss Ratings, has a number of benefits:

- This special type of gold is typically more portable and much easier to trade.

- You’ll have greater privacy when buying and selling.

- It’s far less susceptible to counterfeit or fraud.

- It has the lowest custom fees when travelling internationally.

In fact, there are two very specific “brands” of gold that we like for the best quality and value over the long term.

And I’ve put together a full report that outlines everything for gold buyers called, The Best Way to Buy Gold for a Crisis.

This report is valuable for both gold newbies and long-time gold bugs.

You’ll get our in-depth knowledge of the gold market, acquired over 100 years at Weiss Ratings.

Inside, you’ll learn:

- The two best ways to buy physical gold, as I mentioned above. These are the most fungible, pure and tradeable gold assets you can find.

- I’ll share the names of the nine most trusted dealers in the gold industry. Here at Weiss, these are the only people we would buy gold from.

- I’ll outline the seven different ways to spot a gold scam from a mile away. This is critically important when gold is in a bull market like right now. Because every Tom, Dick and Harry are coming out of the woodwork with a gold deal that’s too good to be true. I’ll show you exactly how to catch these scammers in the act.

But that’s not all.

Owning physical gold is a great way to protect yourself in a crisis.

But with gold running to all-time highs and beyond — I’ll show you how to maximize your profits on gold as well:

Buying digital gold.

According to JP Morgan, individual investors poured more money into the top gold ETF in 2025 than in the past five years combined.

And the surge in gold isn’t showing any signs of easing up.

But it’s not as easy as just grabbing any old gold ETF. There are different tax rules for different investments.

In The Best Way to Buy Gold for a Crisis, I’ll share the number one gold ETF to buy.

It’s liquid. You can trade in and out. And it is the best tracker of gold values.

All of this is in my report, The Best Way to Buy Gold in a Crisis.

But I also want to be clear:

Gold isn’t the only precious metal running hot right now.

In fact, silver can be very valuable in a crisis as well.

It’s hit some major highs in the last year. And we think silver prices could jump even higher.

In fact, silver’s gains outperformed gold’s impressive rise during the 1970’s inflation and the 2008 financial crisis.

I think it’s critical for smart investors to balance their portfolios with gold and silver, before the AI market crashes.

And I put together a brief silver report called, The Best Way to Buy Silver in a Crisis.

It outlines the two best ways to buy physical silver.

And the number one digital silver investment.

From mid-December to mid-January, silver ETFs saw $921.8 million in volume. That’s the heaviest 30-day buying in history.

And I’ll show you the very best silver ETF to buy right now.

Plus, there’s one more bonus I’ve set aside for you … and I think it’s a real game changer.

You see …

My firm has been quietly studying an investment asset that has vastly outperformed stocks … bonds … and real estate …

It has turned average people into millionaires and even multi-millionaires …

… and a potential AI crash could open the ideal window for this opportunity.

Behind the scenes, I’m urging our readers …

… to stake their claim in this asset class because we predict it’s about to rocket even higher.

You’re about to get this same information.

I’ll tell you exactly how to get in with …

The Weird Way to Make Extraordinary Profits in a Financial Crisis.

Yes, the potential is extraordinary.

And, NO, this has nothing to do with shorting stocks or options.

Nor am I talking about Bitcoin …

But I do ask one thing …

It’s okay to warn your friends and neighbors about how bad things are going to get …

But THIS report?

You might want to keep it to yourself and your loved ones.

All three of these reports are yours today, my compliments:

- The Best Way to Buy Gold in a Crisis

- The Best Way to Buy Silver in a Crisis

- The Weird Way to Make Money During a Financial Crisis

All I ask is that you try a risk-free subscription to my Safe Money Report.

Safe Money Report is the flagship monthly newsletter by Weiss Ratings.

It’s been around for over 40 years.

And is home to some of our biggest predictions ever.

In our monthly Safe Money Report, we warn our members about possible threats to their savings and retirement that we believe are right around the corner.

We give them our Safe Money Report model portfolio, including the stocks that are at the very pinnacle of our ratings.

And we provide advance warnings …

You’ve already heard some of the highlights …

Like how we’ve helped readers avoid the tech meltdown ...

Or how, before the collapse of Bear Stearns … Lehman Brothers … Washington Mutual … Citigroup … and Wachovia … we warned our readers …

At the time, we were bold contrarians …

… and history has proven us right …

For over 40 years, Safe Money Report has published lists of the most vulnerable public companies, ETFs and mutual funds … before crisis sent them plummeting.

We’ve also published lists of companies that are most likely to THRIVE in the coming chaos …

We’ve built a track record that has gotten the attention of Barron’s … Forbes … Fortune magazine … The New York Times … and The Wall Street Journal.

They have all recognized our ability to predict market events.

Barron’s wrote that our ratings service is, “The leader in identifying vulnerable companies.”

This is because we’ve built a massive database on more than 52,000 companies and investments.

Our team of analysts, mathematicians, and data scientists use Irving Weiss’s original formulas …

… combined with new formulas and advanced computer models to cut through the financial fog and detect early warning signals.

This is how we were able to accurately predict bank failures in the 1980s … dot-com collapses in the early 2000s … and the Great Financial Crisis of 2008.

For example, during and after the Great Financial Crisis, 465 banks failed, catching millions of Americans off guard. But using our data and ratings, we were able to warn in advance about 464 of those banks.

Yes, before the banks failed.

We missed only one … a stunning 99.8% rate of accuracy.

As you might imagine, ALL the publicly traded banks that failed saw their stocks plunge in value, many to ZERO. Ditto for the stocks of other failed companies.

But Safe Money Report covers more than just stocks …

We also dive deep into protecting and growing your 401(k) and IRA and every kind of investment it contains, not to mention your real estate.

Today, I’m inviting you to join us.

If you choose to join the elite group of Safe Money Report members …

If you step up to be one of us …

… you’ll get the same kind of accurate information others have gotten for over four decades …

Every month, I’ll send YOU our best intelligence …

… to help you navigate the coming chaos.

Safe Money Report goes way beyond helping protect your wealth from an AI crash.

You’ll discover …

Precious metal strategies designed to keep your wealth safe ...

Which sectors of the market to avoid like the plague as the crisis gets worse …

And which sectors to zero in on so you can look back on this day as the time when your nest egg began to grow and grow and grow.

From my 30 years of investing, I can assure you there is always a way to win … to get wealthy … no matter what the markets are doing.

And our mission is to find that way.

As a member of Safe Money Report, our mission is to make sure you know exactly which stocks to buy, and equally important, which ones to sell.

Our goal is that YOU will watch your wealth grow even while others who didn’t heed our warnings begin to panic.

That YOU will get to enjoy the power and freedom that only a small few get to experience.

But I do want to give a fair warning ahead of time …

Safe Money Report is not for everyone.

Some people can’t handle the unvarnished truth about the economy …

Some want to keep their heads in the sand …

And some are, quite frankly, turned off by our plain speak and no-holds-barred approach.

Those people often don’t stick around with Safe Money Report …

But I think you will.

Because we’ve come this far together, I know that you, like me, are a proud American …

Passionate about keeping your God-given freedoms …

And ready to grow the fruits of your labor.

Plus, a membership in Safe Money Report will give you more than just monthly reports …

You’ll be part of a community of like-minded investors with direct access to some of the most powerful investing tools in the world.

With your Safe Money Report membership …

You get total access to the Weiss Ratings to check the safety of your bank. These are the ratings that warned in advance about the bank failures of the Great Financial Crisis with 99.8% accuracy.

You get total access to the Weiss Ratings to check the safety of your insurance company, the ratings that a study by the US Government Accountability Office showed were far more accurate than those of all other ratings agencies.

Just these safety ratings ALONE make it a wise decision to become a Safe Money Report member.

But you get much more.

You also get total access to the Weiss Investment Ratings giving you “buy”/“sell” signals for every stock, ETF or mutual fund you own or may wish to own.

And our investment ratings have a long history of success.

We launched our first stock ratings a few months before the dot-com bust of the early 2000s. At the time, every major firm on Wall Street was touting Nasdaq stocks, urging investors to “buy, buy, buy.”

In fact, according to Zacks Investment Research, over 98% of the ratings issued by Wall Street were “buys.”

But our ratings said exactly the opposite. We gave nearly all Nasdaq stocks a “sell” rating and not a single one got a “buy.”

Sure enough, three years later, the Nasdaq Composite Index was down 75%, and many of Wall Street’s most favorite darlings lost 98%, 99%, even 100% of their value.

Then, at the beginning of 2003, something changed.

Weiss Ratings started to flash a new signal.

In the wake of the tech bubble collapsing in the early 2000s …

Its grades started soaring for a special group of technology companies.

Like NetEase, Inc …

One of the firms who got caught up in the tech bubble.

Most had left them for dead …

The stock was trading for around 60 cents on April 2, 2003 …

When suddenly, Weiss Ratings upgraded them to a Buy.

Just six months later, the stock almost tripled. It went up 284% …

And it’s up more than 22,700% today.

Tyler Technologies was in a similar situation. Its share price fell more than 85% during the dot-com bust …

And even if the stock gained a little bit of steam in the months following the crash …

For the next couple of years, it was mostly going sideways.

But then, surprisingly to the average market observer, Weiss Ratings raised its grade — and made TYL a Buy in April 2003.

Sure enough, over the next year the stock hiked 168% …

Now, it’s up over 12,200% today ...

Consider what happened with Ebix — another software company relegated to the scrap heap of tech failures …

You’ll notice the same pattern repeats once again.

Weiss Ratings issued a Buy on Ebix on April 2, 2003 …

The stock shot up 453% in the 12 months that followed …

That’s almost 5x in just one year …

And between 2003 and 2019 it went on to gain over 12,500%.

Of 1,186 tech stocks we rated a buy at that time, 590 went up ... with an average gain of 377.3%.

Now, to put that into perspective …

During that same time period, the S&P 500 gained only 249% …

Clearly, our stock ratings are a powerful tool, and with your membership in Safe Money Report, you get them all.

You get 24-7 access to ALL 10,000 of our stock ratings, updated daily.

You get the ability to easily create your own, custom watchlist.

So, whenever your bank, your stocks, your ETFs or your mutual funds are downgraded or upgraded, you get an instant alert via email or text.

And never forget: You get our Safe Money Report model portfolio with our picks of the best of the best, based on the Weiss Ratings.

Plus, here’s one more great benefit: You also get our Weiss Ratings Daily, providing critical updates on all of the above in your inbox every morning, seven days a week.

Now, it’s time for the next step …

All I ask in return is a fair fee that covers the expenses of my team’s research and getting the information to you.

That’s normally been $129 a year, which is an absolute bargain …

Especially when you’re getting financial information that could make such a big difference in your life.

That said …

I won’t even ask you for $129 today.

As we both know …

Time is running out.

And I want to get this valuable information into the hands of the right people who understand the dangers of AI and want to protect their wealth as soon as possible.

So, for now, I’m slashing $80 off the fee.

Right here on this page, you can claim your one-year Safe Money Report membership for just $49.

That’s less than 14 cents per day …

I’ve already shown you how this potential AI apocalypse is shaping up to be …

Worse than the Great Depression …

Worse than the dot-com bubble …

Worse than the 2008 Financial crisis …

In fact, it could be worse than all of them combined.

Imagine if on the eve of all these economic calamities …

Someone was warning you.

And showing you how to protect your wealth — before it’s too late.

Our proprietary formulas have done just that.

In every major economic crisis of the last 100 years.

And right now, we’re doing it again.

Please don’t hesitate …

The difference between acting now — or waiting longer … could be massive.

Take advantage of the special offer we’re making today.

Grab a yearly Safe Money Report membership for just $49.

You’ll have 12 months to cancel, at any time, and get your money back.

And you’ll get our critical reports on how to protect your money from an AI-induced crash.

Please, click the button below to review our offer …

Before it’s too late.